Estate Exemptions and Preparing for Policy Change

The current Administration is seeking to extend the Tax Cuts and Jobs Act (TCJA) as it is currently set to be fazed out after 2025. If the TCJA is phased out, there will be changes to estate exemption amounts. The current exemption amounts are $13.99 million per person or $27.98 million per married couple. There is currently a tax bill in Congress that would extend and increase the TCJA, but if this bill does not pass current exemptions would be reduced. If Congress does not act, the new exemptions are effective January 1, 2026 estimated to be to $7 million per person and $14 million per married couple. If the extension to the TCJA is passed, effective January 1, 2026, the exemptions will increase to $15 million per person and $30 million per married couples, with annual increases indexed to inflation. Congress is hoping to have the bill in front of the President by the end of July to be signed.

If you are considering current gifting, you should be aware that the basic exemption must be used prior to using the TCJA amount. If the TCJA is not extended, the TCJA incremental amount will be lost if not used. In other words, if an individual wishes to take advantage of the current TCJA amounts before they expire, and further legislation is not passed, an individual would need to gift in excess of approximately $7 million (the ‘basic amount’) to take advantage of the full $13.99 million exemption amount.

When the Tax Cuts and Jobs Act (TCJA) was introduced, estate planners raised concerns about a potential claw back, i.e., that the IRS potentially might retroactively include lifetime gifts exceeding the post-2025 reduced exemption in a taxpayer’s estate at death. However, on November 26, 2019, the IRS issued regulations establishing the anti-claw back rule, confirming that properly made lifetime gifts using the higher exemption would not be added back into the estate later. This was further clarified in proposed regulations in April 2022, which confirmed for true lifetime gifts(i.e., those where the taxpayer does not retain possession and enjoyment of the transferred asset).

To make this information digestible we have examples of situations that show the effect of taking advantage of estate tax planning under the current laws:

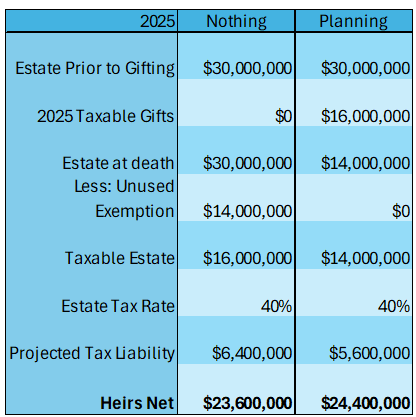

Example 1: Full Exemption

Jack and Joan, both 67, have a combined net worth of $70 million, with a majority held in highly liquid investments.

To take advantage of the current exclusions Jack & Joan plan on making additional gifts to an irrevocable trust prior to December 31, 2025. Jack & Joan then die in 2026. The ‘Planning’ column assumes Jack and Joan fully use the projected exemption, and the ‘Nothing’ column assumes they do not make any gifts prior to death.

While this example shows the worst case with Jack and Joan dying in 2026, it is able to demonstrate the benefits of using current exemptions prior to the December 31, 2025, deadline. Jack and Joan were able to use $14 million more in exemptions without incurring additional tax and give their heirs an additional $5.6 million. If Jack and Joan were to live beyond 2026, they could potentially benefit from inflation increases on the remaining exemption, which may also be offset by the future growth of their estate.

Example 2: Partial Exemption

Debbie and Dan, both 58, are married and have a net worth of $30 million. Roughly half of their net worth is held in Debbie’s closely held business. Debbie has been developing a plan to transition her business to their two children, ages 30 and 27.

Debbie’s business makes giving the entirety of their net worth an unfeasible option. Debbie and Dan are considering using one of their increased exemptions prior to the December 31, 2025 deadline. Debbie and Dan then die in 2026. This is what it would look like if Debbie decides to gift a portion of the nonvoting business stock to an irrevocable trust.

While this example again shows the worst case with Debbie and Dan dying in 2026, it is able to demonstrate the benefits of using current exemptions prior to the December 31, 2025, deadline. Debbie and Dan were able to give their heirs an additional $800 thousand.

Next Steps

If you have any questions or are concerned with potential estate taxes, contact our office at 262-334-3471 to schedule a meeting with one of our Estate Planning attorneys. Our attorneys frequently provide legal services, including estate planning and probate and trust administration, to clients living in West Bend and the surrounding communities of Slinger, Germantown, Kewaskum, Port Washington, Menomonee Falls, Milwaukee, and throughout Washington County, Sheboygan County, Dodge County, Ozaukee County, Waukesha County, Wisconsin.

Originally published: July 30, 2025

More Important Reading

- Giving the Gift of an Education

- Estate Tax Cliff

- Estate Planning for Mixed Families and Second Marriages

Disclaimer: The information contained in this post is for general informational purposes only and is not legal advice. -Due to the rapidly changing nature of law, Schloemer Law Firm makes no warranty or guarantee concerning the accuracy or completeness of this content. You should consult with an attorney to review the current status of the law and how it applies to your unique circumstances before deciding to take—or refrain from taking—any action. If you need legal guidance, please contact us at 262-334-3471 or info@schloemerlaw.com.